How I'm Playing the Permian Gold Rush

How I'm Playing the Permian Gold Rush

The Permian is the hottest thing since sliced bread (and AI), and the latest stock purchase in the Model Portfolio is how I'm playing the Great Permian Land Grab

Like many kids, I grew up as a huge dinosaur / paleontology nerd. Little did I know that this childhood interest would intersect with deep value energy investing, but such is life.

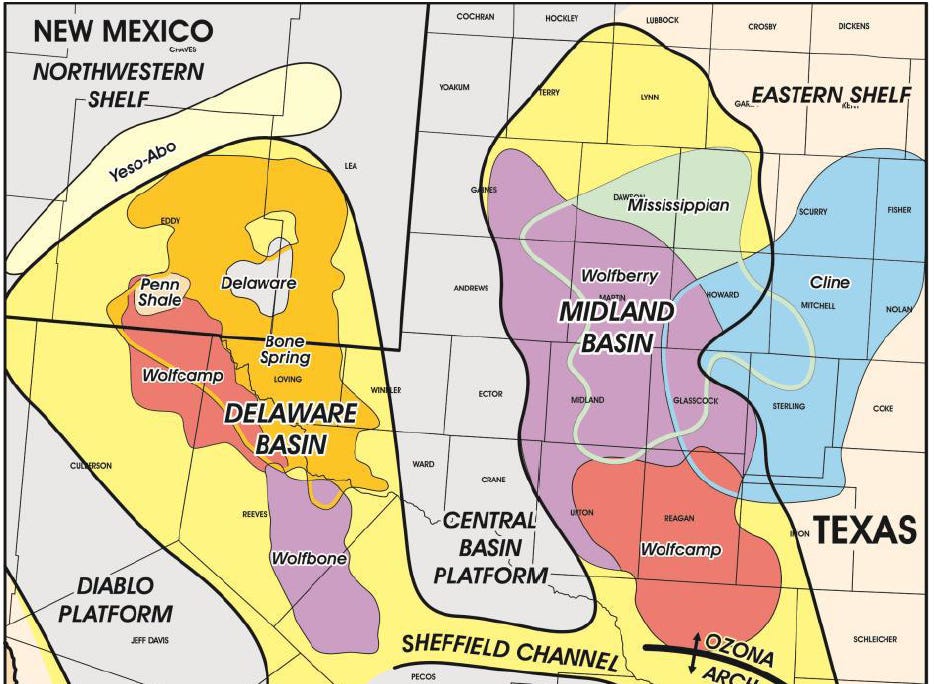

The reason I bring this up is that the Permian Basin, a geological formation in West Texas / Southern New Mexico is the hottest energy play in the world right now, with both oil majors and independent producers rushing to consolidate production and acreage.

The reason for the attractiveness of the Permian is three-fold:

Vertically stacked oil & gas formations in the Permian means that you can hit paydirt at multiple depths over the same acreage via fracking, boosting efficiency

Existing oil & gas infrastructure is excellent, given that oil companies have been operating in the Permian for many decades (conventional drilling, with fracking recently taking over)

Energy-friendly regulatory environment, with most of the acreage held privately (not having to lease from government) and less ESG opposition to drilling vs. many other locations

Incidentally, the Permian Basin is named after the Permian era (which occurred right before the dinosaurs emerged in the Triassic period) as much of the hydrocarbon-laden geological zones were formed during this period.

In any case, the Permian is heating up in terms of M&A activity with a flurry of deals announced in the last 12 months:

Pioneer bought by Exxon

Callon bought by Apache

Hess bought by Chevron

Crown Rock bought by Occidental

Endeavour bought by Diamondback

…and many other smaller deals

This week, another deal was announced with Chord Energy buying out Enerplus. This merger is more focused on the Bakken basin (not Permian) but again shows that M&A activity showing no signs of slowing down in the shale oil patch.

**As an aside, Chord Energy (formerly Oasis Energy) was a very successful investment opportunity I wrote up back in 2021.

So the natural question to ask is, who is the next target to be acquired?

I believe this Permian producer, which I purchased for the Hidden Rock Capital this week, would be a prime candidate for being bought out.

At the same time, I do not want my investment thesis to rely solely on a buyout, and I believe this stock is an attractive stand-alone opportunity trading at a bargain price relative to future earnings, cash flow, production, and reserves.

Let’s dig in!