Whale of a Tale

How I rode a 75-bagger and lived to tell the tale

In my decade plus of investing, I’ve realized that investment performance tends to follow the Power Rule which I paraphrase as the following:

A few big wins drive the bulk of your gains and can outweigh many small losses.

Or to apply the famed Pareto principle:

More than 80% of your gains are driven by less than 20% of your investments.

In my personal investment journey, there has been no investment more impactful than an obscure coal company named Alpha Metallurgical Resources (NYSE: AMR), formerly known as Contura Energy before it was renamed Alpha in 2021.

Incidentally, AMR is also one of several high-conviction picks in the Hidden Rock Capital Model Portfolio, and one that has hopefully made a lot of profits for subscribers!

Since purchasing my initial 500 shares at a cost basis of around ($3.50 per share) in 2020, the stock price has now gone up by roughly 75x to its current price around $260/share.

To put that in context, the $1,750 of AMR stock I purchased 3 years ago is now worth more than $130,000. That’s the Investment Power Rule truly at work!

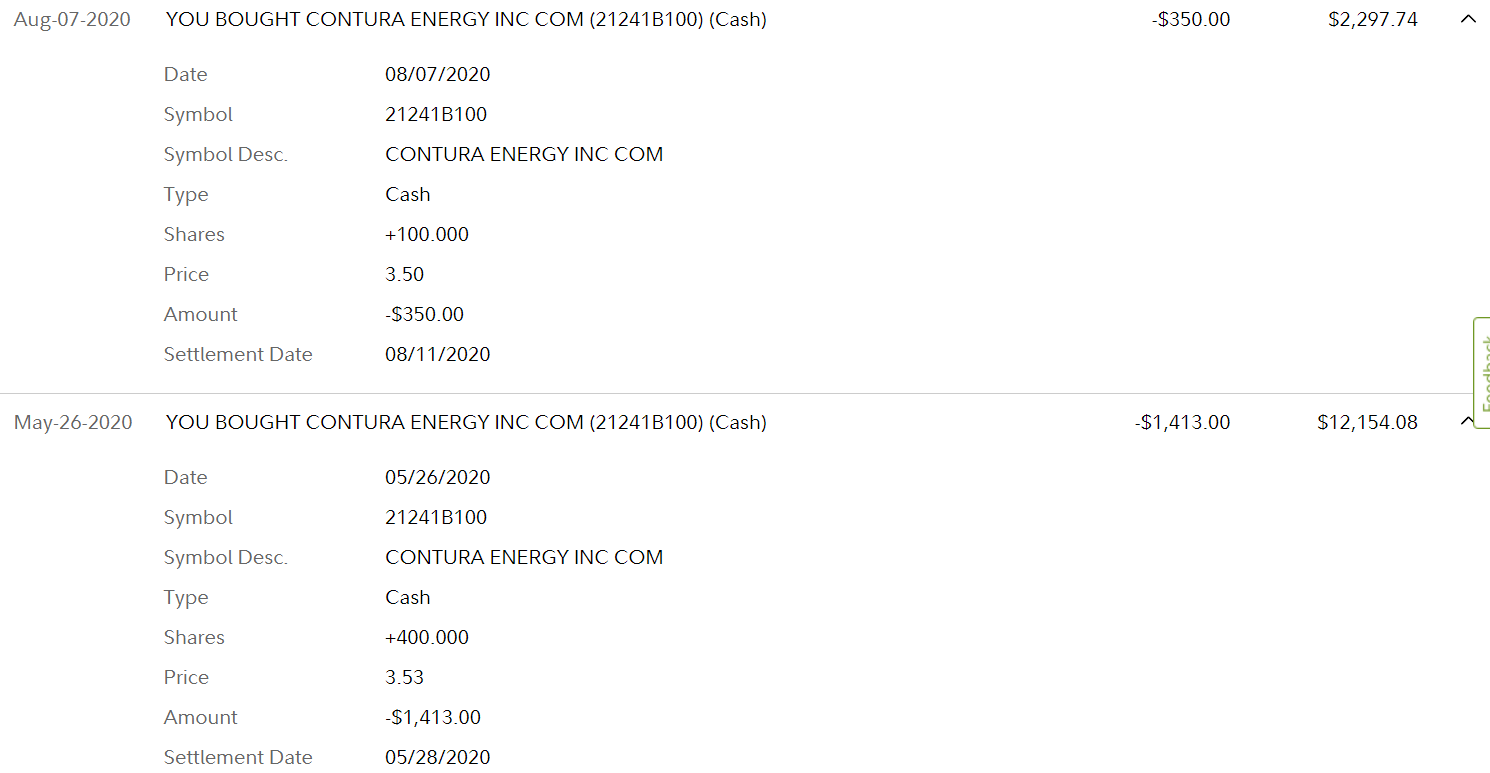

Snapshot of my initial purchase of AMR (called Contura back then) in my personal portfolio is show below as proof. After all, pics or it didn’t happen! 😂

So how did I stumble upon a 75-bagger, and manage to ride it all the way to this point?

Here are the 3 lessons I’d like to share from this whale of a tale:

A lot of money can be made when a stock left for dead starts showing signs of life…

When I first bought AMR in the summer of 2020, the stock was left for dead in the wake of COVID, a significant debt load, and a relatively high cost structure relative to its competitors. Given its checkered history with multiple bankruptcies, the market was pricing AMR stock as an equity stub likely headed for its 3rd restructuring in 10 years.

But with a little imagination (and some luck), you could see even then that the company was doing the right things to address its balance sheet and cost structure so that when the coal price cycle turned, AMR could reap the rewards.

You could also see the coal sector on the cusp of an upwards inflection point given zero planned supply growth, continued resilient demand certainly for metallurgical coal (and even for thermal coal from emerging economies), and an industry cost curve that had marginal production costs way above coal prices back then in 2020… an unsustainable situation for any commodity.

This paradigm shift where investors used to view AMR as an equity stub within a rapidly dying coal industry, to now seeing AMR as a viable going concern with potential decade plus of free cash flows still ahead, drove most of my early returns, from $3.50/share to roughly $60 per share range by late 2021.

This was the first leg of my journey with AMR, and incidentally the most profitable from a pure percentage return perspective.

Luck plays a big part in investing, but you can also position yourself to get lucky!

After a strong 2020-2021, came the Ukraine invasion in 2022 which sent many commodity prices skyrocketing. Coal was no exception, with Russia being a major global supplier.

On the one hand, you could say that I got “lucky” since no one (including me) anticipated Russia invading Ukraine as part of their pre-2022 investment thesis on AMR.

But on the other hand, there is such a thing as positioning yourself to be lucky, in that you invest in asymmetric opportunities that are priced for EVERYTHING GOING WRONG, and not for ANYTHING GOING RIGHT, so that if you have an unanticipated positive catalyst, this can rerate the stock much higher. Similar concept as lesson #1 above.

I believe the coal equities space pre-Ukraine invasion was one such asymmetric opportunity where stocks were priced at 3-4x free cash flow, so that any unexpected positive development such as Russia invading could skyrocket the stock prices much higher.

And that is exactly what happened, with share prices rising from ~$60/share in the beginning of 2022 to touching $180/share by summer of 2022… a triple in the course of just a few months.

This was the second major leg in my rollercoaster ride with AMR.

Sometimes a dirt cheap valuation can be its own catalyst!

After the Ukraine invasion shock to coal supplies became priced in, coal prices and equities experienced a pull-back & consolidation during the back half of 2022 and early 2023.

But this time, armed with significant free cash flow and a rock-solid balance sheet boasting a net cash position, AMR management astutely took matters into their own hands and embarked on an ambitious share buyback program.

Starting from the beginning of 2022 to now, AMR has completed $850M in share buybacks out of $1.2B authorized, taking the share count from 18.6M on March 2022 to 13.7M at end of July 2023…a reduction of almost 30%!

Source: AMR Investor Presentation from August 2023

This buyback program initially did not impact the share price very much, but as they continued to chip away at the float, the stock price eventually started inflecting upwards, with almost a 100% YTD return in 2023.

I have been very impressed by the management team sticking to their guns that AMR stock was “criminally undervalued” and forced an upwards rerating in the stock price by pouring almost all of their discretionary free cash flows into buybacks.

Incidentally this was my major investment thesis on sticking with AMR despite sitting on enormous paper gains, as well as recommending the stock to Hidden Rock Capital subscribers.

I had seen this exact playbook work for another stock in a down-trodden industry - Dillard’s (NYSE: DDS), which has been one of the best performing retail stocks in the past 5 years despite operating in the “dying” strip mall sector.

Other examples where management creates significant value to rerate the stock higher may be:

1) Making significant counter-cyclical investments such as what Exxon and Hess did sticking with the monster Guyana deep water projects through the pandemic oil crash

2) Picking up competitors on the cheap at the bottom of the cycle once they have crashed such as what JP Morgan Chase did with Washington Mutual in 2008 and again with Silicon Valley Bank earlier this year during the regional banking crisis.

AMR management forcing their stock price higher via buybacks is what I attribute the bulk of my returns in this third and final leg of my investment journey, from less than $140/share in the beginning of 2023 to $260/share currently.

While the percentage move higher has not been as large as the first two legs of my journey (<100% gain), because I kept most of my original AMR shares, the actual dollar gain has been the largest during this third leg- exhibiting again the Power Rule at work.

So How does this Story End?

After a 7,500% return from first purchase during the last 3 years, I believe AMR is still a cheap investment with more upside, but probably not my highest conviction pick anymore.

With valuations reaching closer to 5-6x free cash flow (vs. less than 4x FCF earlier this year), downside risk is also increasing, as the coal sector is a hyper-volatile sector that requires ample margin of safety.

That being said, I can certainly see AMR hitting $300+ per share by next year if management continues chipping away at the share count, and the stock is still relatively cheap so this is not necessarily a sell recommendation, but more of a hold.

But for myself, I will likely step off this rocket ship and start trimming AMR shares in both my personal portfolio and also in the Hidden Rock Capital Model Portfolio.

Subscribers who purchased AMR after I first recommended it around $175/share in this post from March 2023 have seen a ~50% gain and hopefully were able to make significant profits.

I love this quote from Trader Ferg about getting out early and missing out on some of the fun at the end in order to protect your downside and continue playing the game.

Knowing when to say “enough” and book a profitable investment implies that you are confident that you can find other future asymmetric opportunities to invest these profits to continue compounding your capital.

That will be my task over the coming months, and I look forward to sharing more compelling opportunities as I find them with my subscribers & readers.

I hope you learned a thing or two from my whale of a tale, and have a great weekend!

Great read. Taking the value here and applying it across commodities.

You mentioned DDS but it's not in your model portfolio. Do you mind elaborating why?